Australia’s future prosperity will depend in large part on its ability to move from being primarily a supplier of raw materials to becoming a more active participant in advanced technology value chains.

Successfully developing new technological capabilities in areas such as artificial intelligence and semiconductors could support more productive industries, higher-skilled employment, stronger wage growth and greater economic resilience. Australia already possesses many of the ingredients required for such a project. The challenge is to identify realistic areas of comparative advantage and pursue them through a coherent national strategy.

Australia’s International Profile

For decades, Australia has benefited from exports of minerals, energy and agricultural commodities, but heavy reliance on extractive industries leaves the economy exposed to dangerous fluctuations in global demand and commodity prices while contributing to a long-term pattern of deindustrialisation.

The point is visible in Australia’s trade profile:

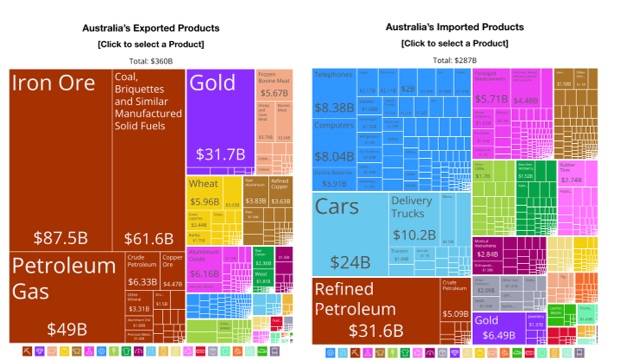

Figure 1. Australia’s exported and imported products in 2024.

Source: Observatory of Economic Complexity (OEC), 2026.

According to the Observatory of Economic Complexity (OEC), Australia’s major exports remain heavily concentrated in iron ore, coal, petroleum gas, gold, wheat and other resource or agricultural products. Its imports, by contrast, include cars, refined petroleum, telephones, computers, electric batteries, delivery trucks, medical products and machinery. This means that Australia often captures value at the extractive end of global supply chains while importing many of the complex goods that embody advanced design, engineering, fabrication and intellectual property.

Australia does, however, have genuine potential advantages to overcome this. It has a strong research university system, world-class mining expertise, abundant critical minerals, a highly educated population, as well as partnerships and economic ties across both the Indo-Pacific and the Western alliance system. These advantages can provide the basis for a national strategy aimed at developing advanced technologies.

New National Strategy

Such a strategy would need to integrate foreign policy, industrial policy, migration policy and education policy. This would mean to move beyond vague slogans about “innovation”, and into a disciplined national project with clear goals, planning, realistic timelines, public investment, private-sector coordination, research institutions, measurable outcomes and periodic review. Market actors alone are unlikely to make long-term, uncertain investments in technological capability without policy support.

In this sense, specific policies should be considered as interconnected elements of a broader strategy:

Foreign policy should be treated as an instrument of industrial development. Australia occupies a rare position within the emerging technological order (it is a formal security ally of the United States, deeply integrated into Indo-Pacific trade networks, and a major supplier of critical minerals required for advanced manufacturing). This position creates opportunities that Australia has not yet fully leveraged. The United States is seeking trusted partners for semiconductor supply chains through initiatives such as the CHIPS and broader economic-security partnerships. Australia should ensure that its growing strategic contributions are accompanied by tangible industrial benefits, including technology transfer, joint research programs, advanced manufacturing investment, workforce development, and the localisation of selected segments of semiconductor design, testing, packaging and supporting services. China is investing heavily in semiconductor manufacturing while remaining Australia’s largest trading partner. Australia could pursue areas of mutual economic interest that support domestic capability-building, including processing industries, research collaboration, advanced manufacturing investment and infrastructure development. This would mean to approach both partners as potential sources of capital, technology, expertise and industrial partnerships.

Industrial policy would then need to push Australia beyond extraction. The immediate priority should not be full-scale leading-edge chip fabrication, which remains extraordinarily capital-intensive and dominated by a small number of global firms. More plausible opportunities lie in areas adjacent to Australia’s existing strengths: compound semiconductors, photonics, sensor technologies, quantum-related hardware, critical-mineral processing, chip-design support, advanced packaging, secure data-centre infrastructure, and specialised AI applications in mining, agriculture, health and energy. This would require public finance on a much larger and more strategic scale than conventional grants alone. Australia already has useful instruments, including the National Reconstruction Fund, Export Finance Australia, the Critical Minerals Facility, and the new Critical Minerals Production Tax Incentive. These tools should be treated as the beginning of an industrial strategy. A more ambitious approach would link resource extraction directly to industrial upgrading. Australia could reform royalty and resource-rent arrangements so that part of the revenue generated from non-renewable mineral exports is channelled into a sovereign industrial capability fund dedicated to critical-mineral processing, semiconductor-adjacent manufacturing, advanced equipment acquisition, and early-stage technology firms. Rather than simply taxing exports etc., the system could reward domestic value-adding through concessional finance, production credits, procurement guarantees, equity stakes, and common-user processing facilities. In selected strategic areas, public equity or even state-owned enterprises should not be ruled out, particularly where the market is unlikely to build patient, capital-intensive capabilities on its own. The aim would be to convert Australia’s mineral endowment into productive capacity, rather than allowing it to leave the country mainly as unprocessed geological wealth.

Migration and education policy are equally important. A semiconductor and AI strategy is ultimately a talent strategy, but Australia’s migration system is not yet sufficiently integrated with a broader industrial project. Existing instruments already point in the right direction: the National Innovation visa is designed to attract exceptional talent, while regional skilled visas and employer-sponsored pathways seek to direct labour toward specific areas. These tools should be more explicitly aligned with strategic sectors such as critical-mineral processing, advanced manufacturing, AI infrastructure, semiconductor-adjacent industries, energy systems etc. Doctoral scholarships, industry-linked fellowships, vocational training places and permanent residency pathways could be targeted toward engineers, computer scientists, materials scientists, technicians, project managers and experienced manufacturing workers. This would also require rethinking the role of regional migration. Current working holiday and student visa arrangements often supply labour to agriculture, hospitality and low-complexity service sectors. Those pathways could be complemented by a more ambitious stream of “strategic regional work” linked to industrial zones. Work in critical-minerals projects, processing facilities, advanced manufacturing precincts and related infrastructure could receive stronger recognition in points-tested migration and permanent residency pathways. Regional universities, TAFEs and technical institutes should be funded to support this strategy through scholarships, industry placements and applied research partnerships. The aim would be to attract and retain skilled and semi-skilled workers in the regions where Australia’s next stage of industrial development is most likely to occur (e.g. Western Australia), rather than treating migration primarily as a short-term labour supply for existing low-wage sectors.

Certainly, this is no easy task and would require political coordination, patient public investment, resistance to lobbying by sectors that benefit from the status quo etc. The alternative, however, might also be risky if that means to remain a wealthy but structurally dependent economy that exports minerals, imports technology, and hopes that service-sector growth can absorb the social pressures generated by housing costs, insecure work and weak productivity. Australia has the ingredients for a more ambitious path, and what it lacks is a sufficiently coherent industrial project.

Caio Gontijo is an Associate Lecturer at the University of Wollongong. His research focuses on international relations, international political economy, and the changing dynamics of the international order. He has recently published in leading international journals including International Affairs (2026) and International Studies Review (2025).

This article is published under a Creative Commons license and may be republished with attribution.